Press Release

CBRE analysis: The subletting trend is slowly but surely starting to affect the industrial and logistics real estate market in Czechia

July 18, 2024

The domestic industrial real estate market experienced a real "boom" during the coronavirus pandemic. The record growth of interest in renting new premises, especially from companies linked to e-commerce, triggered extensive speculative construction. However, after two extraordinary years, there was a slowdown in demand last year, which continues this year as well. Although the market situation is stable and positively influenced by the gradual reduction of construction costs in combination with the stabilisation of yields, in recent months there has been a slight increase in the vacancy rate and the emergence of two new phenomena on the market. CBRE, a world leader in the field of commercial real estate services, analyses the growing trend of subletting and targeted maintenance of some properties by developers in the shell & core state.

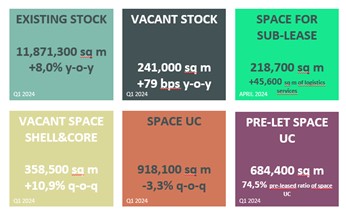

“Weakening demand for online shopping has led to a sudden drop in related logistics services and warehousing. Given that the standard length of a lease agreement for industrial properties is around five years, some tenants found themselves in the unenviable situation of having overcapacity almost overnight. As part of the solution, some of them then decided to sublease vacant spaces," commented Lukáš Šaling, Head of Advisory & Transaction for Industrial and Logistics at CBRE, who continued: "This approach has the potential to have a negative effect on the vacancy rate and the amount of rent in some locations. Some of the inquiring companies prefer subletting, usually at a lower price, to securing their own premises. According to our statistics, the current offer of such areas is already 219,000 sq m, while approximately 241,000 sq m are available for standard rent. However, the good news is that the domestic market is on a good footing, and the trend of subletting has not significantly affected it yet."

Another side effect of the pandemic can be seen directly among developers, who in recent years have increasingly engaged in speculative construction. Now they have part of these spaces unoccupied. "However, instead of formally reporting the premises as empty, they prefer to preserve them in a shell & core state, i.e. just before the completion of the rough construction. In this way, they can offer them for rent in an almost final form, but with the possibility of quick modifications in the order of three to six months according to the needs of specific tenants," described Šaling, adding: "However, such behaviour distorts the view of the current situation on the market, since these spaces, which by the end of the first quarter increased by 10.9% to 358,000 sq m, do not affect current construction, newly completed premises or vacancy in the statistics. Accordingly, the vacancy rate appears lower than it actually is."

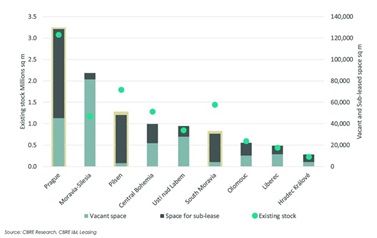

At the end of the first quarter, the total vacancy rate of industrial real estate in the country was 2.03%. At the same time, the mentioned trends manifested themselves to different extents in different regions. "The increased ratio of subletting to the vacancy rate is particularly noticeable at the main logistics hubs, i.e. in Prague, Pilsen and the South Moravian Region. It is also evident in Olomouc, Hradec Králové, the Central Bohemian Region and Liberec. However, all these regions are very resilient due to their size and popularity among tenants. From the market indicators, we see only a slight shift in the vacancy rate in percentage units (below 5%) within the entire Czech Republic," said Šaling.

A significant part of the offers consists of temporary and short-term solutions, largely satisfying the needs of 3PL companies, i.e. distribution and/or storage. The reason is simple: these spaces are usually pre-equipped with the tenant's technologies, and thus any major layout modifications are limited. This also greatly limits the variety of potential tenants.

In any case, the key problem with industrial subleases remains their prediction. Unlike offices, where owners usually offer subletting on behalf of their tenants, in industrial real estate they are often advertised by the companies themselves, sometimes without the knowledge of the owner. This makes it difficult to monitor the market situation and provide a comprehensive overview. “Some listings can be active for months before they are taken off the market, others fill up so quickly they are almost unnoticeable. In any case, owners or potential investors should monitor the situation carefully. The type of sublease is decisive: for example, a 3PL company can base its business on subletting space and offering logistics services, while another company will only offset high costs in this way. All these factors subsequently play a role in the adequate valuation of the building," described Lukáš Šaling, concluding: "As one of the suitable solutions for how the owners can solve this situation, I recommend taking over these unused spaces under their own management and, thanks to this, controlling demand and the amount of rent in the locality.”

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.