Press Release

CBRE Analysis: Domestic retail continues to grow moderately, gaps between sectors widen

May 26, 2026

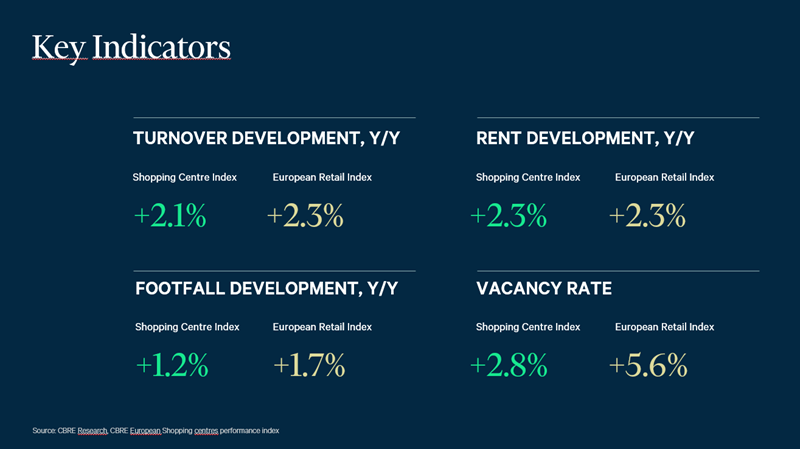

- Attendance at regional shopping centres increased by 1.2% year-on-year in 2025

- Turnover recorded a year-on-year growth of 2.1%

- The vacancy rate fell to 2.8%

- Average rent increased by 2.3% year-on-year

The just-published Shopping Centre Index – an annual assessment of the performance of regional shopping centres by real estate consultancy CBRE – shows that domestic retail maintained stable performance in 2025. The index also includes a customer survey that monitors how people's behaviour is changing when searching for and evaluating shopping centres.

"Last year's data shows the market in good shape: the vacancy rate of shopping centres fell to a historic low, the average turnover rate accelerated year-on-year, visitor numbers stabilised and rents increased. However, differences between individual sectors and types of centres are increasingly apparent under the aggregate figures. The format and composition of tenants – not just the location itself – also determine the outcome. A centre in a smaller town with a well-designed mix can outperform a shopping centre in a large city that has lagged behind market developments," comments Jana Prokopcová, Head of Research at CBRE.

Attendance and occupancy: a solid foundation that is not a given

"Attendance is no longer automatic and directly reflects what shopping centres actually offer—that is why they must actively address it. Those that invested in the tenant mix and customer experience benefited more last year. The rest stagnated at previous levels," describes Jana Prokopcová. On average, attendance at regional shopping centres increased by 1.2% year-on-year. At the same time, the centres achieved an exceptionally low vacancy rate of 2.8%, which is almost half the European average (5.6%) and demonstrates the structural strength of the Czech market over the long term.

Tenant mix: slow but visible reshuffling

The largest part of shopping galleries is still occupied by fashion, with a share of approximately 37%. Although the overall shopping centre mix seems relatively stable, there is a reshuffling of tenants within individual categories. The greatest expansion last year was recorded in Food (+14%), which includes wine shops, delicatessens, bakeries, tea rooms, and organic and health food stores, followed by Services (+10%) and Household & Furniture (+6%). A specific phenomenon is pet stores—in the Czech Republic they account for 2% of all stores in shopping centres, approximately five times more than in Germany. Another emerging trend is higher-quality used and vintage stores, which are now gaining ground in the Czech Republic.

Turnover and rents: acceleration with reservations

Overall turnover at regional shopping centres increased by 2.1% year-on-year on average last year, while rents rose by 2.3%. Both values are slightly below inflation, which indicates persistent pressure on the real profitability of tenants and landlords. The strongest performance was recorded by Electronics (+6.5%), Leisure (+5.2%), and Sports (+3.5%). Food & Beverage as a whole grew by 2.8%, with coffee shops and ice cream outlets performing best (+10.7%), restaurants growing by 5.5%, and fast food slowing to 3.5%. Fashion recovered after a decline in 2024 (+1.2%), with structural changes taking place within the segment: men's apparel turnover grew by 15.5% and young apparel by 7.1%, while women's apparel declined. The biggest drop was recorded in Services (−5.6%)—the 10% expansion of space was not accompanied by a corresponding increase in sales. Household & Furniture also recorded a decline (−2.1%).

The type of centre is decisive: format and tenant composition as a competitive advantage

The data shows that the performance of individual centre formats varied. Malls with a dominant food tenant fared best—they improved their turnover by 3.4%. Experience-oriented centres recorded an increase of 2.3%. Inner-city centres showed an increase of only 0.4%. Shopping centres with a dominant food tenant or a diverse range of gastronomy and services also achieved higher attendance and longer customer stays. "A centre that can offer a reason to stay longer—a combination of food, services, leisure, and a quality environment—has a better starting position. And it's not just about attractiveness for the customer, but also about negotiating power with tenants, who are now carefully choosing where to expand," explains Jan Janáček, Head of Retail Sector and A&T at CBRE.

Blending of online and offline sales: traditional indicators are losing their informative value

The share of online sales in total tenant sales ranges between 17% and 20% and is growing by approximately 1.5% year-on-year. Part of shopping centres' sales therefore flows into online channels. The brick-and-mortar store increasingly functions as a showroom—the customer tries out the goods on site, but buys them online. The real value that the store creates for the brand and the centre is therefore not fully reflected in the reported sales. "Today, turnover per square metre does not reflect the tenant's real situation as accurately as it used to. The customer doesn't care which channel they buy through. If we want to understand what's really happening in the centre, we need to monitor the results in individual sales channels and their role in the entire purchasing chain," says Jan Janáček and adds: "Stores are also increasingly becoming a key part of the logistics infrastructure as delivery points for e-shops. People who come to the centre only to pick up an online order may seemingly distort the statistics on overall traffic in the shopping centre, but for the other tenants they represent a fundamental opportunity. They bring purchasing potential that can be leveraged. It then depends purely on the tenants' skill and the attractiveness of their offer whether they can appeal to this visitor and motivate them to spend more."

Customer survey: convenience determines visit, experience determines mall selection

A survey of almost 1,200 customers shows that customer behaviour is not changing dramatically, but gradual changes are clearly visible. The frequency of visits over the past two years reflects the polarisation of the market: 51% of respondents are not changing their attendance, 30% are visiting malls less often, 10% more often, and 8% prefer closer alternatives. Those who have reduced their frequency most often cite time savings and the availability of online shopping or retail parks as the reasons. A typical visit lasts one to two hours. However, the share of shorter, targeted visits lasting from thirty minutes to an hour is growing.

The most important factors when choosing a mall are a wide range of products under one roof, availability close to home or work, parking, and speed of shopping. "Comfort determines whether a customer will come at all. The quality of the experience determines which shopping centre they ultimately choose when they have a choice. In an environment of growing competition from retail parks and online shopping, this factor is crucial," says Jan Janáček, adding: "Awareness is not built with one campaign. Centres that ignore social networks and optimisation for artificial intelligence tools will become invisible to the youngest and most dynamic groups of Generation Z customers, aged 18 to 25."

Retail parks and market structure: the Czech Republic in bronze in the European Union

While the construction of new shopping centres is stagnating—major new projects are expected only from 2027 in Prague, Brno, and Pardubice—retail parks continue to expand dynamically. In 2026, approximately 90,000 m² of new space is expected to be completed.

With a density of 194 m² of retail parks per thousand inhabitants, the Czech Republic ranks third in the European Union, approximately 50% above the average. Retail parks in the country account for 45% of the total retail stock, significantly exceeding the European Union average of 35%. The Czech Republic's purchasing power index stands at 92 (EU = 100), meaning there is less purchasing power per square metre of retail space than the European average.

For shopping centres, this combination means the end of price competition in the traditional sense. The future lies in differentiation—in offering a mix of tenants, experiences, gastronomy, and community functions that a retail park, by its very nature, cannot provide. “Retail parks today are not an alternative format—they are part of the entire retail ecosystem. This, combined with below-average purchasing power, means that the market will become more sharply divided. The market is closing quickly for average shopping centres,” says Jan Janáček, adding: “This year will fully demonstrate which centres can respond to how customers actually shop—across brick-and-mortar stores and online channels. Anyone waiting for a return to the old ways may be waiting in vain.”

About the Shopping Centre Index

The CBRE Shopping Centre Index is the only market indicator that has continuously monitored the performance of regional shopping centres in the Czech Republic since 2013. This year's 14th edition analyses a sample of 22 shopping centres in the regions (excluding Prague) with a retail area exceeding 650,000 m², representing 39% of the total volume of regional shopping centres, over 2,100 tenants, sales of around CZK 31 billion and 102 million visits per year. The index also includes a customer survey conducted in April 2026 on a sample of almost 1,200 respondents.

About CBRE Retail

CBRE is an expert in retail space management and currently manages 22 shopping centres and retail parks in the country. It provides extensive and comprehensive advice on the purchase and sale of retail assets, the leasing of retail space, representing tenants entering the Czech market, optimising store networks, and the management, marketing, and concept design of shopping centres and retail parks. Last but not least, it is a leader in retail market research and customer behaviour analysis.

About CBRE Group, Inc.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services. The company has more than 155,000 employees serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, critical infrastructure); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.