Press Release

25 years of CBRE in the Czech Republic: How has the commercial real estate market changed over the past quarter of a century and where is it headed next?

November 18, 2024

CBRE, the world leader in commercial real estate services, is celebrating 25 years on the domestic market. During this period, the market underwent significant changes and matured into a stable investment environment that can withstand international competition and attract domestic and foreign capital.

Clare Sheils, Managing Director at CBRE Czech Republic, states: "While initially transactions were mainly dominated by office properties, interest in other sectors increased over time: whether it was retail, industrial and logistics, hotels or emerging investment assets."

The heads of individual departments specialised in specific segments of commercial real estate commented on the main factors that have most influenced the current market and reflecting on its future prospects.

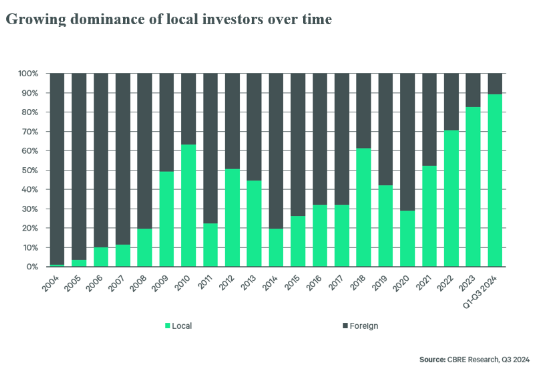

"The past quarter of a century has been defined by several significant milestones. From the point of view of the development of the investment market, the entry of the Czech Republic into the European Union in 2004 was absolutely essential. It significantly increased the confidence of foreign investors and brought new investment opportunities. Overcoming the financial crisis of 2008 was also a turning point. Although it dampened investment activities for three years, the market ultimately came out even stronger. Moreover, it was at this time that local investors began to appear and gain influence," commented Jakub Stanislav, Head of Investment Properties at CBRE.

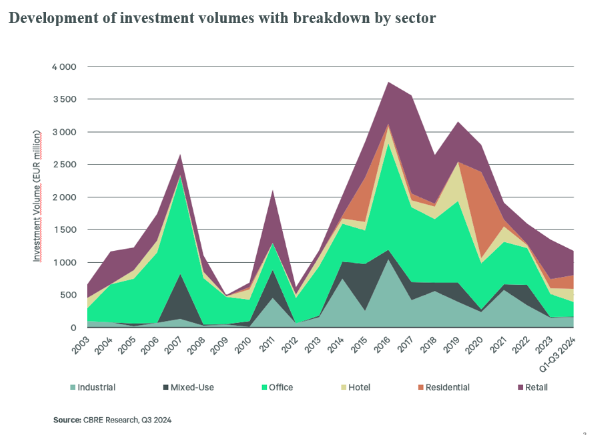

The years 2016, 2017 and 2019 were historically the strongest. On average, around 1.9 billion euros are invested in the country per year, but in these years the total volume of investments broke the 3-billion mark. Although similarly high volumes cannot be expected in the near future, the market is in good shape and has the potential for further growth.

"Transactions have long been dominated by standard commercial sectors, i.e. offices, shopping centres or industrial and logistics real estate. However, in recent years, investors have begun to place a greater emphasis on portfolio diversification in order to minimise the risks associated with economic fluctuations. Due to this, interest in investing in alternative segments such as rental residences, student campuses and medical facilities is growing. At the same time, the sustainability of projects is gaining importance. Energy certificates and international certifications such as BREEAM or LEED are becoming a key criterion when evaluating investment opportunities," stated Stanislav.

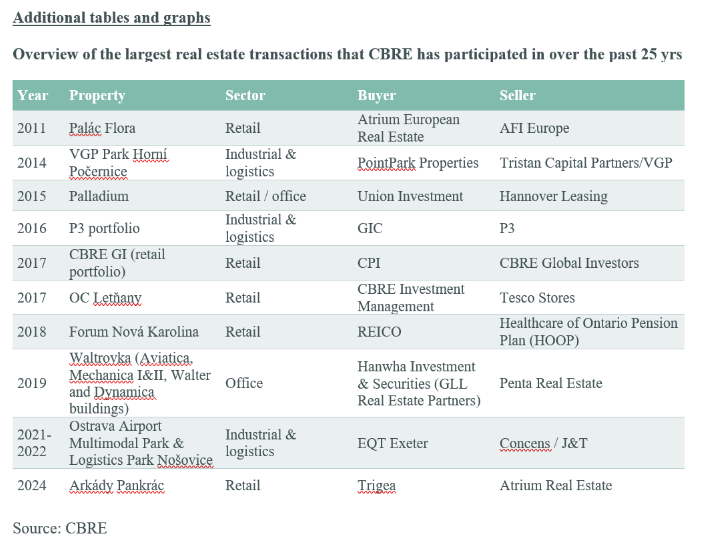

CBRE was behind a number of the largest transactions carried out on the domestic real estate market

Whether it was the sale of the shopping centres Palladium, Palác Flora, OC Letňany, Arkády Pankrác, Forum Nová Karolina, logistics parks across regions or even the Waltrovka office complex, CBRE was part of it.

Changes in the office market: discovering new locations, work models and coworking

In 1999, when CBRE opened its domestic branch, 1.3 million sq m of office space was available in Prague, almost a third of which was right in the centre. Since then, significant office hubs have started to emerge, of which the metropolis currently has eleven. Whether it is Pankrác-Budějovická, Karlín or other locations, the total leasable area has tripled to the current 3.9 million m². During the past years, we have experienced an incredible boom in digital tools and technologies such as video conferencing, cloud services or various collaborative platforms that simplify the work of individuals and at the same time enable remote teams to function. This created the basis for the growing popularity of shared offices and coworking centres, which currently account for 4% of the capital's total office space. The demand for them is constantly growing, as is the expansion of their operators.

However, despite all these key moments, 2020 can be marked as a turning point for the office segment. The onset of the Covid-19 pandemic significantly affected the current form of work and accelerated the transition to hybrid models. Companies are now putting more emphasis on the health and overall comfort of their employees, while they are more motivated by meaningful work, company culture, opportunities for professional growth and greater flexibility than just a salary.

"The Prague office market has already recovered from the pandemic and thus proved its resilience. The vacancy rate now stands at 8.1%, which is the lowest among the capital cities in the CEE region. Going forward, we expect the market to continue to adapt to new work models and technological innovations. At the same time, flexibility, sustainability and employee health will continue to be key factors influencing the shape of workplaces," explained Helena Hemrová, Head of A&T Office at CBRE, adding: "Previously, long-term leases of 5 to 10 years were common. Today, there is a greater demand for more flexible contracts, often for 3 to 5 years with the option of an extension. Modern leases also contain clauses allowing tenants to adapt the premises to their current needs, whether it is the possibility of subletting, returning part of the premises or additional building modifications.”

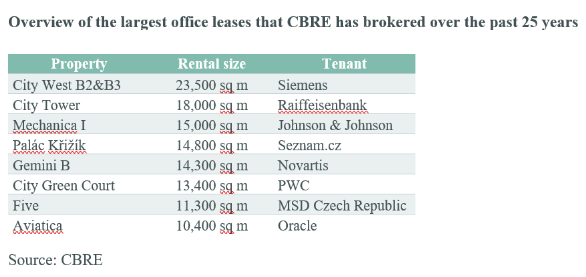

CBRE has been involved in the mediation of thousands of square meters of offices over the past 25 years

Among other things, it provided space for the Raiffeisenbank headquarters in the City Tower building in Pankrác, the Siemens headquarters in the City West B1 and B2 buildings in Stodůlky, the Johnson & Johnson headquarters in the Waltrovka complex in Jinonice, the facilities of the Seznam.cz internet portal in the Křižík Palace in Smíchov, and the pharmaceutical company MSD in the Five and Riverview buildings, also in Smíchov.

Retail in the thick of things: from the arrival of foreign chains to the expansion of shopping centres to digitisation

Since 1999, the area of shopping centres in the country has increased more than eightfold to the current 2.6 million sq m. At the same time, the market has undergone significant changes that reflect the wider economic and social transformations following the Velvet Revolution. This dynamic development has included several key phases and trends that have fundamentally affected the way consumers shop and how retailers operate their stores.

After the fall of communism, when modern retail was mainly represented by department stores Kotva, Máj, Bílá labuť and Prior, the market began to quickly open up to foreign investors. Large international chains such as Tesco, Carrefour, Ahold (formerly Mana, now Albert) and Kaufland entered the country. These players brought with them new business models, a wide range of goods and modern technology, which significantly improved the offer and quality of services. At the end of the millennium and in the first decade of the 21st century, there was a significant development of hypermarkets and shopping centres, which changed their offer over the years. At first, the developed centres were dominated by a hypermarket with an attached shopping mall, after which the mall, which offered a wide selection of goods, was expanded, followed by entertainment and gastronomic services. This trend has changed the shopping habits of customers who have started to prefer one-stop shopping.

With the development of the Internet and modern technologies, the era of e-commerce started, and popular online retailers such as Alza and Mall gradually began to compete with traditional brick-and-mortar stores. At the same time, digitisation has led to the introduction of new payment methods, loyalty programs and personalised offers, further attracting customers to online shopping. Their significant increase occurred mainly during the Covid-19 pandemic. Movement restrictions and social distancing have brought new challenges to retailers and accelerated some changes in the market. Many brands have had to adapt their business models and invest in digital solutions to remain competitive.

"The current condition of the retail market is good and this is evidenced by the very low vacancy rate of around 4%, but we still feel the reverberations of the post-Covid period, which was quickly followed by a phase of steep inflation growth. The footfall of shopping centres is still not up to 2019 levels (by 5%), which was considered to be the strongest ever in retail. Sales have already surpassed 2019, but inflation had a significant effect on this," commented Jan Janáček, Head of A&T Retail at CBRE, adding: "Current market developments are very dynamic and require retailers to quickly adapt to customer requirements, which, in addition to the smooth connection between standard and online sales channels, also includes the involvement of modern technologies, including AI, and an emphasis on sustainability. In recent years, this has become one of the key aspects in the construction of new shopping centres, but also in the operation of existing ones."

CBRE helped with the expansion of a number of foreign brands on the Czech market

Whether on the side of the landlords or in the form of the exclusive representation of brands during their expansion, CBRE participated in the expansion of the offer of domestic shopping centres and luxury boutiques on the high street. It helped brands such as Samsung, Tous or Palmers, as well as Versace and Ralph Lauren, enter the Czech market.

The transformation of the logistics market: the development of infrastructure, the inflow of foreign investment and the rise of e-commerce

The industrial and logistics real estate market has developed significantly over the past 25 years in terms of size, and the number of developers and tenants operating on it. This year, in the 3rd quarter, the total volume of leasable area reached 12.1 million sq m, of which 2.6 million were completed in the last three years.

The foundation for this growth was laid by the entry of the Czech Republic into the European Union, which, with the help of European funds, led to the construction of an extensive infrastructure. A new network of highways and railways made access to industrial zones easier, starting an inflow of foreign investment, especially from Germany, Japan and South Korea. "Although it may seem that the construction of domestic highways is progressing slowly, their network has almost tripled in recent years. While in 1999 it included 502 km of highways, at the beginning of this year it already amounted to 1,388 km," explained Jan Hřivnacký, Head of Industrial Leasing at CBRE.

The state and regional governments also played a big role in the development of industrial and logistics zones by actively supporting their creation and thereby attracting new investors. Investments in modern technologies and automation, which increased the competitiveness of Czech industrial companies, also had an influence. Significant milestones that defined today's market include the establishment of the development company CTP and its dynamic growth in regional cities, the acquisition of America’s Prologis in Rudná, the sale of a portfolio of 11 logistics parks jointly owned by Tristan Capital Partners and VGP to P3, as well as the construction of the first distribution centre of an American internet store with global scope in Dobrovíz, which was developed by Panattoni.

"The e-commerce boom during the Covid-19 pandemic was completely unprecedented, leading to a significant increase in demand for logistics and storage space. We are currently in a situation where the record years 2021-2023, which contributed very significantly to the development of the market, are behind us. These years saw the highest demand for industrial space, the lowest recorded vacancies and the highest activity in terms of construction. Two "big-box" transactions for an area of around 200,000 sq m were also concluded. Transactions of this size are truly unique on the Czech market and we are glad that we were able to participate in both," said Hřivnacký, concluding: "After this extraordinary period, the market is gradually returning to normal, pre-Covid levels. Compared to the record years, we are observing reduced demand, a slight increase in vacancies and the associated decrease in rents and an increase in incentives. The market is starting to be dominated by demand from manufacturing companies, which in the end could also support the growth of logistics."

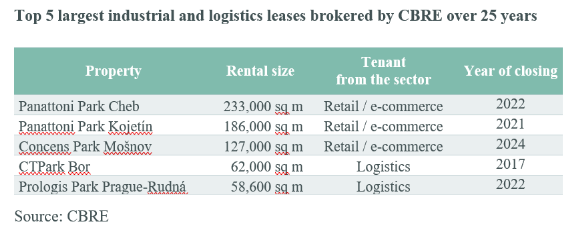

CBRE contributed to the development of important industrial and logistics zones in the Czech Republic

It stood by developers during the creation of a number of important industrial and logistics zones across the country, especially in the vicinity of Prague, Brno, Ostrava and Pilsen. CBRE also brokered tenants for key players on the domestic market, whether it is CTP, Panattoni or P3.

CBRE Group, Inc. (NYSE: CBRE), a Fortune 500 and S&P 500 company headquartered in Dallas, is the world’s largest commercial real estate services and investment firm and a premier provider of critical infrastructure services (based on 2025 revenue). The company has more than 155,000 employees (including Turner & Townsend employees) serving clients in more than 100 countries. CBRE serves clients through four business segments: Advisory (leasing, sales, debt origination, mortgage servicing, valuations); Building Operations & Experience (facilities management, property management, flex space & experience, data center solutions); Project Management (program management, project management, cost consulting); Real Estate Investments (investment management, development). Please visit our website at www.cbre.com.